Credit Scores: The Invisible Gatekeeper When Buying a Home

Credit scores are a sticky subject when it comes to buying a home. Maybe you’ve made some mistakes in your younger years, or you had an income gap resulting in some late payments that you’re trying to clean up now. Maybe you’ve played it safe and have used your credit responsibly. Maybe you have some manageable credit card debt that you’re worried is holding you back.

When buying a home, your credit score does a lot of heavy lifting in how you become (or don’t become) approved for a mortgage. Your score directly impacts interest rates and other factors involved with the process, like what kind of loan you qualify for.

Let's break it down.

What is a credit score, really?

Your credit score is a three-digit number, typically between 300 and 850, that represents how reliably you've managed debt in the past. Lenders use it to predict how likely you are to repay a loan in the future.

The most commonly used model is the FICO score, though you may also encounter VantageScore. For homebuying purposes, FICO is what matters most and mortgage lenders will actually pull three separate scores (one from each major credit bureau: Equifax, Experian, and TransUnion) and use the middle number for their decision.

Your score is built from five factors:

- Payment history (35%): Have you paid your bills on time?

- Credit utilization (30%): How much of your available credit are you using?

- Length of credit history (15%): How long have your accounts been open?

- Credit mix (10%): Do you have a variety of credit types (cards, loans, etc.)?

- New credit (10%): Have you recently applied for new credit?

Payment history and utilization make up nearly two-thirds of your score, which tells you where to focus your energy.

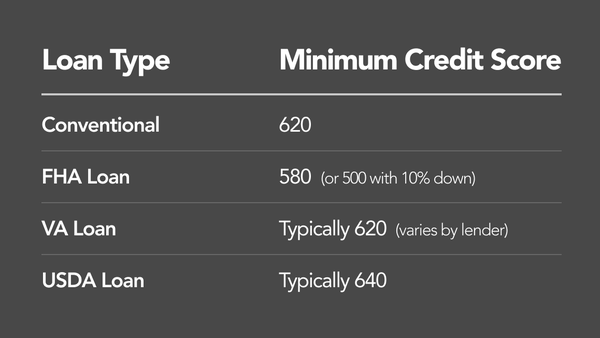

What credit score do you need to buy a home?

There's no single answer, it depends on the type of loan you're applying for.

These are minimums, not targets. Getting approved with a 620 is possible. Getting good terms with a 620 is a different story.

Which brings us to the part most people don't talk about enough.

How your credit score affects your mortgage rate

Your credit score doesn't just determine whether you get approved, it determines what you pay for the life of your loan.

Here's what that looks like in real numbers. On a $300,000 30-year fixed mortgage:

- 760+ score: ~6.5% interest rate → ~$1,896/month

- 700–759 score: ~6.75% rate → ~$1,946/month

- 640–699 score: ~7.25% rate → ~$2,047/month

- 580–639 score: ~7.75% rate → ~$2,151/month

The difference between a 760 and a 620 is roughly $250 per month, or about $90,000 over the life of the loan. That's a real financial consequence of a number most people don't think about until they're already in the process.

This is why your credit score isn't just a hurdle to clear. It's a lever that directly affects how much homeownership actually costs you.

How to improve your credit score before you buy

The good news: credit scores aren't fixed. They respond to your behavior, and with the right moves, you can see meaningful improvement in 6–12 months.

Pay on time, every time. This is the single biggest factor in your score. Even one missed payment can cause a significant drop. If you struggle to remember due dates, set up autopay for at least the minimum on every account. If something happens and you need more time to pay, contact your credit card company, they may give you an extension so you’re not reported as late to the credit bureaus.

Get your utilization below 30%. If you have a $5,000 credit limit and you're carrying a $2,500 balance, your utilization is 50% and that's hurting your score. Paying balances down (or requesting a credit limit increase without spending more) can move your score faster than almost anything else.

Don't close old accounts. It feels counterintuitive, but closing a credit card, especially an old one, may hurt your score by shortening your credit history and reducing your available credit. If you're not using a card, consider leaving it open with a small recurring charge on it.

Hold off on opening new credit. Every time you apply for a new credit card or loan, it creates a hard inquiry on your report. A few of these in a short window signal risk to lenders. In the 6–12 months before you plan to buy, keep new applications to a minimum.

Check your credit report for errors. Mistakes happen like accounts that aren't yours, payments incorrectly marked as late, balances that haven't been updated. You're entitled to a free credit report from each bureau annually at AnnualCreditReport.com. Review it and dispute anything that looks off. Even one error can drag your score down meaningfully.

What to do with this information

Your credit score is one of the most powerful numbers in your homebuying journey but it's not a verdict. It's a snapshot of where you are right now, and it can change.

The buyers who end up with the best mortgage terms aren't necessarily the ones with the highest incomes. They're the ones who started paying attention early. They understood that a few months of intentional credit management could be worth tens of thousands of dollars over the life of their loan.

If you don't know your score today, find out. If it's not where you want it to be, start building a plan. The earlier you start, the more options you'll have when your HomeOwner Day arrives.